Costs are very important in business decision-making. Cost of production provides the floor to pricing. It helps managers to take correct decisions, such as what price to quote, whether to place a particular order for inputs or not whether to abandon or add a product to the existing product line and so on.

Ordinarily, costs refer to the money expenses incurred by a firm in the production process. But in economics, cost is used in a broader sense. Here, costs include imputed value of the entrepreneur’s own resources and services, as well as the salary of the owner-manager.

There are various concepts of cost that a firm considers relevant under various circumstances. To make a better business decision, it is essential to know the fundamental differences and uses of the main concepts of cost.

Accounting and Economic Costs:

Money costs are the total money expenses incurred by a firm in producing a commodity. They include wages and salaries of labour; cost of raw materials; expenditures on machines and equipment; depreciation and obsolescence charges on machines; buildings and other capital goods; rent on buildings; interest on capital borrowed; expenses on power, light, fuel, advertisement and transportation; insurance charges, and all types of taxes.

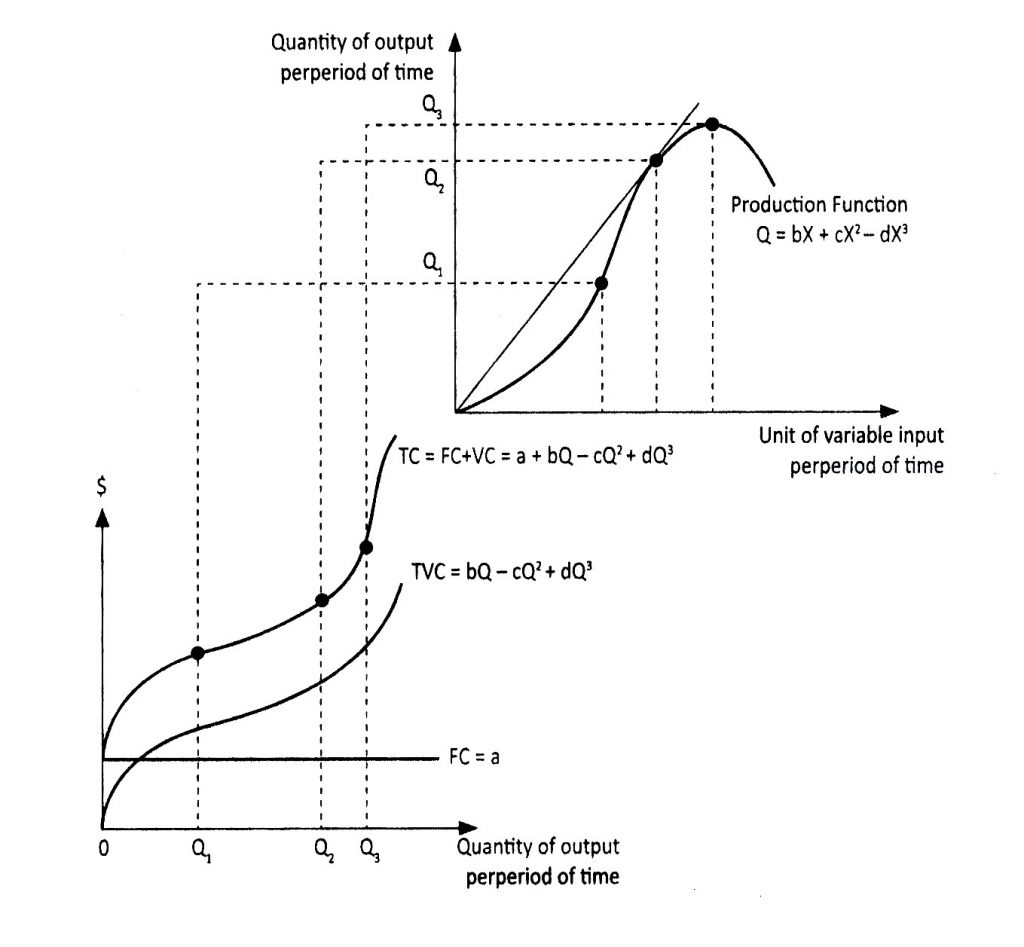

source:

Cost Theory: Introduction, Concepts, Theories and Elasticity | Economics